| Component | Q4 2025 (vs Q3) | Q1 2026 (vs Q4) |

|---|---|---|

| DDR5 RDIMM (Server) | +53% to +58% | +88% to +93% |

| LPDDR5X (Mobile) | +43% to +48% | +88% to +93% |

| NAND Flash | +20% to +60% | +33% to +100% |

The global memory chip market is currently undergoing a significant structural adjustment. From server memory to mobile flash storage, contract prices and spot quotations across multiple product categories have risen rapidly in Q1 2026. For professionals responsible for hardware procurement and infrastructure planning, understanding the driving forces behind this volatility and the capital market’s medium-term forecasts is more valuable than focusing on short-term price figures.

Price Increases: The Supply-Demand Reality Behind the Data

| Company | 2023 | 2024 (est/revised) | 2025 (Projected) | 2026–2028 Outlook |

|---|---|---|---|---|

| Samsung | Highest (approx. $44B) | Slightly lower/Stable (prioritizing profitability) | Significant increase expected | Investing $41B+ in new Korean fabs (P5) by 2028 |

| SK Hynix | Low ($8.3B - 56% decline) | High (approx. $15.9B - up 91%) | Very high (focused on HBM/DRAM) | ~$75B total through 2028; Includes $15B+ new Yongin/Cheongju fabs |

| Micron | Low ($7.7B) | Moderate ($8.4B) | High ($15.8B+) | ~$20B in FY26; Massive expansion in Idaho/NY (2026-2028) |

According to joint monitoring data from Counterpoint Research and TrendForce, mainstream memory products experienced varying degrees of price increases between February and March 2026: Contract prices for server-grade 64GB DDR5 RDIMM showed quarter-over-quarter increases of 80%-95%, while mobile LPDDR5X and laptop DDR4 SO-DIMM also recorded significant upward movement. NAND flash products followed suit, with enterprise SSD contract prices generally rising in the 30%-50% QoQ range.

It’s important to note that these figures primarily reflect contract procurement prices rather than retail spot market quotations. For enterprise procurement, contract price trends carry greater significance as they directly impact bulk purchasing costs and annual budget planning. The current price increases are driven not by short-term speculation, but by systematic rebalancing of supply-demand dynamics within the technology iteration cycle.

Capacity Reallocation: How AI Demand is Reshaping Supply Patterns

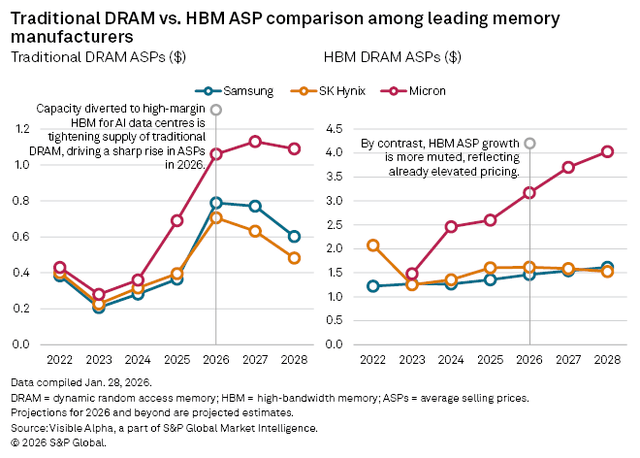

The underlying logic of this round of memory market changes stems from the concentrated absorption of high-end memory resources by AI infrastructure. High Bandwidth Memory (HBM), as a core component of AI training and inference servers, delivers 5-8 times the wafer value compared to traditional DDR5. Against this backdrop, the three major manufacturers—Samsung, SK Hynix, and Micron—have unanimously tilted their capital expenditure and capacity planning toward HBM and advanced packaging technologies.

SK Hix explicitly stated in its 2026 investor briefing that its DRAM capacity expansion will “prioritize ensuring supply stability for HBM3E and HBM4.” Samsung’s DS Division similarly emphasized in its quarterly earnings call that “capacity allocation will focus on high value-added products rather than simply pursuing bit shipment growth.” This strategic contraction has directly slowed the growth of new supply for commodity DRAM (such as standard DDR5 and LPDDR5X), while demand from enterprise servers and high-end laptops continues to expand, creating a supply-demand gap.

Capital Expenditure: Medium-to-Long-Term Supply Curves Under Cautious Expansion

Facing industry-wide losses from the oversupply conditions of the previous cycle (2023-2024), major memory manufacturers have demonstrated a remarkably consistent cautious approach in this recovery phase. Although Micron has announced long-term capacity planning totaling approximately $200 billion across Idaho, New York, and other U.S. locations, most of these projects are not expected to contribute actual output until the second half of 2027 through 2028. Samsung and SK Hynix’s capital expenditure increases are also significantly lower than historical cycle peaks, with funding priorities directed toward advanced process nodes and packaging rather than simple replication of traditional wafer capacity.

This “quality over quantity” capital strategy has significantly reduced supply elasticity in the memory industry. Gartner noted in its March 2026 report: “Current memory capacity construction cycles have extended from the traditional 12-18 months to 24-30 months. Coupled with geopolitical factors affecting equipment delivery, short-term new supply cannot quickly respond to demand fluctuations.”

Market Forecasts: Dual Variables of Cycle Duration and Structural Divergence

Regarding the duration of this memory upcycle, capital markets and industry research institutions share some consensus while maintaining key divergences. The mainstream view suggests that, assuming AI infrastructure investment momentum does not significantly cool, supply-demand tightness for high-end memory products may continue through mid-to-late 2027. The inflection point for commodity product prices, however, depends on the recovery pace of consumer electronics demand and the flexibility of manufacturers’ capacity reallocation.

Notably, references to “shortages lasting until 2028” in some overseas media often originate from contexts indicating that “the current super cycle may see supply-demand rebalancing or 阶段性 oversupply in 2028,” rather than a linear continuation of shortage conditions. This distinction in phrasing reminds us that when interpreting industry forecasts, attention must be paid to the complete context and data boundaries of original sources.

From a capital market perspective, the valuation logic for the memory sector is shifting from “cycle speculation” to “technology premium.” Morgan Stanley noted in its February 2026 semiconductor industry report: “Manufacturers with HBM mass production capabilities and advanced packaging technologies will achieve higher earnings certainty and valuation premiums in this cycle.” This judgment indirectly validates the rationality of manufacturers’ strategic pivots.

Closing Thoughts As a foundational element of digital infrastructure, memory chip price volatility and supply pattern changes are essentially the result of dynamic interplay among technological evolution, capital allocation, and market demand. For enterprise procurement and IT planning teams, when developing medium-to-long-term hardware strategies, understanding structural signals behind capacity cycles, technology roadmaps, and capital expenditures is as important as monitoring immediate quotations. In a market environment where uncertainty has become the norm, maintaining continuous tracking of industry dynamics may prove more valuable than predicting the next price inflection point.

This briefing synthesizes information from Counterpoint Research, TrendForce, DIGITIMES, The Register, and official disclosures from Samsung, SK Hynix, and Micron. Data current as of March 2026.